Compounding fears over the UK economy, PM Johnson delivered a speech that promised changes to the current Brexit deal that if were not met would lead to a No-deal Brexit 31st October. Tesco were unchanged after they announced their CEO would be stepping down next year. He had previously been seen as the person that took a struggling Tesco and turned them around but a wider slow down in the sector tarnished initial success. “Retail bosses are like football managers, a handful of names always moving around the top jobs, notching maybe a season or two of success before inevitably failure catches up with them.” wrote Markets.com analyst Neil Wilson on the departure of Tesco’s boss. The biggest fallers on the FTSE 100 were Kingfisher (-6.8%), Hargreaves Lansdown (-5.9%) and AB Foods (-5.1%) in late afternoon London trade.UK #construction PMI at 43.1 in September – that’s territory consistent with a sharp contraction in output. Decline in new work volumes also point to a weak end of year – despite the efforts of the public sector balance sheet to prop up demand

— Simon French (@shjfrench) October 2, 2019

Equity markets sink on growth concerns and Brexit worries

Equity markets sank around the world on Wednesday as a string of poor economic data combined with fears over Brexit to shake the confidence out of markets.

The FTSE 100 was down over 190 point or 2.6% to 7161 in afternoon trade which culminated in the worst start to October since 2014.

A series of poor global economic date raised fears companies were going to struggle through earnings season.

“It’s going to be a tough season and the most important thing will be how the companies view going into Q4 and the early outlook for 2020, which is shaping up to be a tough year for markets and corporates,” said Neil Campling, analyst at Mirabaud Securities.

The market has digested a broad set of manufacturing data which has pointed to to deterioration economic activity and could possibly signal wider economic strife.

Topps Tiles Q4 results hit by weak consumer confidence

Topps Tiles (LON:TPT) said on Wednesday that like-for-like sales declined during its fourth quarter, impacted by a difficult economic climate.

Shares in the UK’s largest specialist supplier of tiles were down during trading on Wednesday morning.

The British retailer said that, in the fourth quarter, like-for-like sales decreased by 1.9%, blaming the “more challenging economic backdrop”, with uncertainty hitting consumer sentiment.

Matthew Williams, Chief Executive Officer, said that “political uncertainty continued to weigh on consumer confidence in the final quarter and we expect this to remain a feature until there is greater clarity”.

Indeed, as the nation has now entered the month of the extended Brexit deadline, the only certainty that prevails is additional uncertainty.

Just last week the Supreme Court ruled that Boris Johnson’s prorogation of Parliament was not only unlawful but also ineffective and non-existent.

Topps Tiles added that it expects adjusted revenues for the full year to be in the region of £214 million, and adjusted pre-tax profits for the year are expected to be within the range of current market estimates (£15.5 million to £16.0 million).

“Despite continued tough market conditions it has been a year of significant strategic progress for the Topps Group,” the Chief Executive Officer commented in a company statement.

“In Retail, the recent launch of our new, industry-leading website brings new levels of inspiration to our customers and further integrates our digital and in-store offer,” the Chief Executive Officer said.

“In Commercial, our investments in building the salesforce, opening new design studios and improving its digital capabilities have enabled Parkside to establish significant momentum in its second year within the Group.”

Topps Tiles also saw its sales dip first quarter of the financial year, amid what it described as a “challenging market backdrop”.

Shares in Topps Tiles plc (LON:TPT) were trading at -6.50% as of 09:49 BST Wednesday.

Ryanair passenger volumes up 8%

Ryanair revealed its passenger volumes for the month of September on Wednesday.

Shares in Ryanair were down during Wednesday morning trading.

The low budget Irish airline said that it flew 8% more passengers in September.

Passenger volumes for the month increased to 14.1 million, up from the 13.1 million figure recorded in 2018.

Earlier this year, Ryanair posted a 21% fall in first quarter profits. It highlighted Germany and the UK as its weakest markets – the latter as a result of the prevailing Brexit concerns on consumer spending.

The airline faced baggage-policy chaos in 2018, altering its baggage policy twice in one year. It dramatically reduced the amount of free luggage that passengers are able to take on board with them.

Elsewhere in the aviation industry, the British global travel group Thomas Cook recently collapsed, leaving thousands of British holidaymakers stranded abroad.

Customers and employees took to Twitter to share their experiences and thoughts. Meanwhile, some Thomas Cook customers accused other airlines of capitalising on the collapse – the BBC reported that in some instances, the prices of replacement flights have tripled.

The Civil Aviation Authority said this week that is launching a new process for what will be the largest ever ATOL refund programme for Thomas Cook customers who had an ATOL protected holiday booked with the collapsed airline in the future.

The largest peacetime repatriation, “Operation Matterhorn”, was launched last week by the Civil Aviation Authority to bring stranded Thomas Cook customers back to the UK.

Shares in Ryanair Holdings plc (LON:RYA) were trading at -1.86% as of 09:54 BST Wednesday.

Tesco CEO to leave in summer 2020

Tesco (LON:TSCO) said on Wednesday that its CEO, Dave Lewis, has decided to step down from his position.

Shares in Tesco were up during trading on Wednesday.

The Group CEO is set to depart from the business in the summer of 2020, Tesco said on Tuesday in its interim results.

Chairman John Allan added that “we have appointed Ken Murphy to succeed Dave as Group CEO of Tesco next summer.”

The British supermarket and general merchandise retailer also revealed that profit before tax for the half year amounted to £494 million, rising 6.7%.

Tesco said that it is now well-positioned to continue to be highly competitive “in challenging markets”.

“Despite challenging external conditions we have delivered a very good start to the year,” Dave Lewis said.

“I’m very pleased to say that we have now delivered every element of the turnaround plan and from this position of strength, the transformation of our business continues at pace,” the Chief Executive continued.

“My decision to step down as Group CEO is a personal one. I believe that the tenure of the CEO should be a finite one and that now is the right time to pass the baton,” Dave Lewis commented on his resignation.

“Our turnaround is complete, we have delivered all the metrics we set for ourselves. The leadership team is very strong, our strategy is clear and it is delivering. The Tesco brand is stronger and customer satisfaction is the highest it has been for many years. Colleagues are doing an extraordinary job and their expertise shows in every store and channel every day.”

Earlier this year, the British supermarket chain reported a slowdown in sales growth in the first quarter.

It also revealed a 34% rise in full-year profit earlier in April.

Shares in Tesco plc (LON:TSCO) were trading at +2.17% as of 09:26 BST Wednesday.

China’s systemic tipping point: Hong Kong protester shooting and CPC’s 70th anniversary

Today the world winced as Hong Kong authorities shot the first pro-democracy protester. Contemporaneously, China marked the 70th anniversary of the Communist Party’s rule with a jingoist tour de force and a cliche comic-book-villain-esque speech from Xi Jinping, who lauded the ‘unstoppable rise of China’. The resulting ominous aura following today’s developments was likely caused by the impression that China has no intention of maintaining either the regional or international status quo.

After succeeding in blocking the extradition bill, Hong Kong’s pro-democracy lobby has since upped the ante against looming Chinese influence, with escalating violence in clashes with authorities. Today, though, the stalwart opposition to authoritarianism may have had a taste of things to come, with a teenage protestor being shot in the chest from point-blank range by a police officer.

Speaking on the incident, the Hong Kong police chief commented,

“At about 4pm, a large group of rioters attacked police officers near Tai Ho Road, and they continued with their attack after officers warned them to stop. As an officer felt his life was under serious threat, he fired a round at the assailant to save his own life and his colleagues’ lives.”

“The round hit an 18-year-old, and the area near his left shoulder was injured, and he was conscious when taken to Princess Margaret Hospital.”

“The police force really did not want to see anyone being injured, so we feel very sad about this. We warn rioters to stop breaking the law immediately, as we will strictly enforce the law.”

Responding to the shooting and what appears to be a sentiment of limited remorse from Hong Kong authorities, Amnesty International issued the following statement,

“The shooting of a protester in Hong Kong marks an alarming development in the police’s response to protests.”

“We call on the Hong Kong authorities to launch a prompt and effective investigation into the sequence of events that left a teenager fighting for his life in hospital.”

“We are urging the Hong Kong authorities to urgently review their approach in policing the protests in order to de-escalate the situation and prevent more lives being put at risk.”

Unfortunately, things will likely worsen before they improve. On the one hand, you have a highly educated and prosperous populace, who will not soon relinquish the democratic rights that have been afforded to them, and will actively resist pernicious (and perhaps soon more overt) influence being exerted by China. On the other hand, you have a growing, hungry dragon, already being poked by Donald Trump. Already at loggerheads with their rival for global hegemony, China won’t take kindly to resistance on its own doorstep, let alone in an area that gives it a strategic foothold in the world of financial services. Beyond that, though, China’s willingness to heavily intervene in its own economy and put on a military parade belonging in a bygone era, shows us that its intentions go well beyond money.

When Xi Jinping talks about the unstoppable rise of China, he is referring to dominance in all spheres. After decades of oppressing its own people (including a case being brought before the European Court of Human Rights this week, with China being accused of harvesting organs from falsely imprisoned Islamic minorities) and making strides toward extending its influence on a global scale (most audaciously with its role in the Hinkley power station and the Hong Kong Exchange’s bid for the London Stock Exchange a few weeks ago), the race to build a ruthless, unified and nigh-on dystopian superpower is well under-way, and the fact that Hong Kong protestors haven’t been quelled with extreme prejudice is – in my opinion – nothing short of remarkable.

No doubt hoping his compatriots will continue fighting the good fight, pro-democracy activist Lee Cheuk-yan told Sky News,

“Today we are out to tell the Communist Party that Hong Kong people have nothing to celebrate.

“We are mourning that in 70 years of Communist Party rule, the democratic rights of people in Hong Kong and China are being denied. We will continue to fight.”

What happens in the coming weeks could potentially set a precedent for future political conflict. If China extinguishes the voices Hong Kong – a small chrysalis of modern free market liberalism – it could potentially throw down a gauntlet that lets the West know that it will go well beyond tariffs, if necessary.

Elsewhere in political and macro economic news, there have been updates from; the Supreme Court’s ruling, the collapse of Thomas Cook (LON: TCP), ECB stimulus, the bid for the London Stock Exchange (LON: LSE), Lloyds Banking Group PLC (LON: LLOY), Jo Johnson quitting, Hilary Benn’s Brexit delay bill, Barclays (LON: BARC) and Deutsche Bank (ETR: DBK).

Severfield reinforces its foundations with Harry Peers acquisition

Structural steel producer Severfield plc (LON: SFR) announced it had entered into an agreement to wholly acquire structural steel work business Harry Peers and Co Limited.

The deal announced today was valued at a total consideration of £30.4 million. The Company said an initial cash consideration of £18.0 million would be financed through cash reserves and a term. The remaining £12.4 million will comprise of cash and cash equivalents. Severield then said a conditional £7 million performance-based deferred consideration is in place, which would be paid by late 2020 should ‘certain financial and operational targets’ be met.

The Group added that Harry Peers commands a respected position within a niche area of the nuclear and defence sectors. Over the next few years, the Company is expected to continue its focus on blue chip customers and is expected to grow on the back of the UK Government’s decommissioning investment programme.

Severfield comments

Alan Dunsmore, Chief Executive Officer, added his insight on the acquisition,

“This acquisition will help Severfield continue to deliver on its strategic objectives. Harry Peers’s experience in specialist, highly regulated, non-cyclical markets will enhance our future growth plans through expanding the Group’s capabilities and sector reach.”

“We believe Severfield is best placed to help Harry Peers continue its profitable growth trajectory, through increased scale and investment and together with Harry Peers’s strong management team we have a real opportunity to develop a broader position within the UK structural steel services market.”

The Company’s statement added,“The Board of Severfield believes that the long-term investment profile of Harry Peers’s key market positions in the highly regulated markets of nuclear, process industries and power generation, enhances its areas of expertise and broadens its market exposure.”

“With the scale and capabilities of the Group, there are substantial opportunities to grow Harry Peers through a number of combined operational initiatives such as new business development functions for Harry Peers, European contract opportunities, and investment in technology-driven enhancements.”

Investor notes

The Company’s share price rallied modestly by 0.084% or 0.060p to 71.16p per share 01/10/19 12:06 BST. Peel Hunt analysts have reiterated their ‘Buy’ stance on Severfield stock, their p/e ratio is 10.69 and their dividend yield stands at 3.94%. Elsewhere in construction and development news, there have been updates from; Billington Holdings PLC (LON: BILN), Epwin Group PLC (LON: EPWIN), Ashtead Group plc (LON: AHT), SIG plc (LON: SHI), Alumasc Group plc (LON: ALU), Somero Enterprises Inc (LON: SOM) and Barratt Developments Plc (LON: BDEV).ScS sitting pretty despite difficult summer

UK-based home furnishing retailer ScS Group PLC (LON: SCS) booked consistent full-year progress across its sales indices, despite a challenging market climate.

The Company’s gross sales improved by £5.8 million year-on-year, to £333.3 million. This drove revenue growth of £4.6 million to £317.4 million, which in turn saw its underlying EBITDA rise by £0.6 million to £19.7 million, and its underlying operating profit bounce 4.6% to £14.3 million.

ScS shareholders enjoyed similar progress, with underlying EPS jumping 13.1% to 30.3p and a full-year dividend of 16.70p per share, up 3.1%.

The Group added that it had opened a new store in Kirkcaldy in September, alongside the roll-out of its in-store sales app in July and further investment in its e-commerce offerings, which saw online sales hike 21.7% to £16.8 million during FY19.

ScS comments

David Knight, Chief Executive Officer, responded to the positive results,

“I am delighted to report another year of good progress and growth for ScS in our continued effort to ensure we remain Britain’s best value sofa and carpet retailer.”

“Since the start of the current financial year, trading conditions have been more challenging, with like-for-like order intake falling 7.6% for the period from 28 July 2019 to 29 September 2019. This period was impacted by the record temperatures experienced by the UK across the August bank holiday weekend and the increasing political and economic uncertainty we are currently facing in the UK.”

“We remain conscious of the impending Brexit deadline, and the impact this may have on the market, consumer confidence and the wider economy. However, the Group’s financial health has never been as strong and with our resilient, debt-free balance sheet, we are in a good position to manage the ongoing uncertainty, and furthermore seek opportunities which will add value in the longer term.”

“Our strong and clear value offering has proven successful, and we are confident it will continue to appeal to our customers who want to buy great products at the lowest possible price.”

Investor notes

The Company’s shares have dipped 6.33% or 15.00p to 222.00p per share 01/10/19 13:07 BST. Peel Hunt analysts reiterated their ‘Buy’ stance on ScS stock, the Group’s p/e ratio is 8.84 and their dividend yield is generous at 7.30%. Elsewhere in retail and on the highstreet, there have been updates from; McColl’s Retail Group PLC (LON: MCLS), Boohoo Group PLC (LON: BOO), Burberry Group plc (LON: BRBY), Associated British Foods plc (LON: ABF), H&M (STO: HM-B) and Sports Direct International Plc (LON: SPD).WPP appoints Sainsbury’s John Rogers

WPP (LON:WPP) said on Tuesday that it will appoint Sainsbury’s (LON:SBRY) John Rogers as Chief Financial Officer.

Shares in WPP were up during trading on Tuesday.

John Rogers is currently the Chief Executive Officer of Sainsbury’s Argos. In this position, he has supervised the digital transformation of the business.

In his role at Sainsbury’s Argos, John Rogers was a contender to take over from Mike Coupe, the CEO of Sainsbury’s.

Moreover, John Rogers was Chief Financial Officer of Sainsbury’s from 2010 to 2016.

Last week Sainsbury’s announced that it had experienced an improved sales momentum across all business areas, whilst also revealing that it will be opening and closing many supermarket, Argos and convenience stores.

WPP said that John Rogers will join its multinational advertising and public relations business in early 2020 and will receive an annual salary of £740,000.

“John is not only an accomplished CFO, but also a leader with extensive experience of business transformation,” Mark Read, CEO of WPP, said in a statement.

“His priority will be to lead a finance function that best fosters investment in creativity, technology and talent in support of WPP’s new strategy for growth,” the CEO continued.

“I am really excited to be joining WPP as it embarks on the next stage of its evolution. As a technology-driven business with creativity at its heart, joining WPP was an opportunity impossible to resist and I look forward to playing my part in helping the business deliver its new strategy,” John Rogers commented on his appointment.

Shares in WPP plc (LON:WPP) were trading at +1.08% as of 13:44 BST Tuesday.

Shares in J Sainsbury plc (LON:SBRY) were also up trading at +1.00% as of 13:45 BST Tuesday.

JD Sports’ Footasylum deal under additional investigation

JD Sports (LON:JD) said on Tuesday that its £90 million deal to acquire Footasylum (LON:FOOT) will undergo an additional investigation.

The leading trainer and sports fashion retailer in Britain agreed to purchase Footasylum earlier this year in a £90 million deal as its smaller rival struggled for survival amid a gloomy trading environment.

The Competition and Markets Authority claimed earlier this month in a Phase 1 decision that the acquisition of Footasylum would “give rise to a realistic prospect of a substantial lessening of competition”.

JD Sports said that it believes there is “clear evidence” that the deal would not lead to a substantial lessening of competition in the sports clothing and footwear retail market.

However, the Competition and Markets Authority confirmed on Tuesday that the deal will now be referred to a Phase 2 investigation.

In response, JD Sports has agreed to co-operate fully with the Competition and Markets Authority in its review to ensure that both retailers will continue to trade in a competitive environment following the deal.

JD Sports highlighted the challenging trading conditions to hit the UK retail market. It emphasised that its rationale behind the deal was “to retain Footasylum’s position as a multichannel retailer, both on the UK high street and online”.

“The CMA has referred their review of this acquisition to Phase 2 on the basis that it could be bad for competition and may have an impact on price,” Peter Cowgill, Executive Chairman of JD Sports Fashion Plc, said in a company statement.

“I strongly disagree with this. This transaction will not result in any price increases or a reduction in product ranges or service quality,” the Executive Chairman continued.

“The focus of all of our Group businesses is to ensure we deliver a best in class, multichannel experience to our consumers by offering a compelling product proposition.”

Shares in JD Sports Fashion plc (LON:JD) were trading at -0.98% as of 12:05 BST Tuesday.

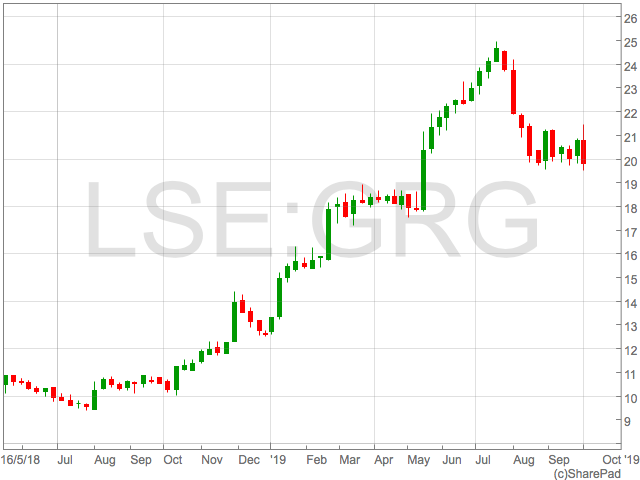

Greggs on a roll in Q3

Greggs said in a Tuesday trading update that it has continued to trade “very strongly” during the third quarter.

For the 13 weeks to 28 September, total sales were up 12.4% and company-managed shop like-for-like sales increased by 7.4%.

The British bakery chain added that its autumn menu is now available in stores. It features new additions to its hot sandwich range, such as Chipotle Chilli Steak and Hot Peri Peri Chicken Baguettes.

Its autumn menu also welcomes the return of its popular Spicy Chicken and Pepperoni Bake, in addition to its Pumpkin Spice Latte.

Greggs added that it is preparing for the potential impact of the UK’s exit from the European Union by stockpiling ingredients and equipment.

Meanwhile, its expectations for the full year remain unchanged.

Earlier in May, the British bakery chain Greggs raised its profit forecasts for the third time this year, driven by the popularity of its vegan sausage roll.

“With over 2,000 Greggs outlets now under its belt, the bakery-turned-food on the go chain, is still on a roll and very much on track for a strong year,” Emma-Lou Montgomery, associate director from Fidelity Personal Investing’s share dealing service, commented on Greggs’ third quarter trading update.

“On its new autumn menu are some seasonal favourites among Greggs customers, like Pumpkin Spice Latte, alongside new offerings such as hot sandwiches and a post-4pm meal deal, as part of the chain’s expansion into all-day dining,” Emma-Lou Montgomery continued.

“Brexit also pops up as an item. But Greggs says it continues to build stores of key ingredients and equipment to ensure its operations aren’t disrupted. This is a company that has its costs under control and its plans in the pipeline, ready to serve up another year of growth.”

The British bakery chain said, however, that it sees food prices going up and sales growth slowed compared to the first half, largely down to the vegan sausage roll being introduced in January. Shares have currently fallen over 5%.

Shares in Greggs plc (LON:GRG) were trading at -6.75% as of 11:18 BST Tuesday.

The British bakery chain said, however, that it sees food prices going up and sales growth slowed compared to the first half, largely down to the vegan sausage roll being introduced in January. Shares have currently fallen over 5%.

Shares in Greggs plc (LON:GRG) were trading at -6.75% as of 11:18 BST Tuesday.

Shares in Greggs (LON:GRG) are up heavily over the last year.

The British bakery chain said, however, that it sees food prices going up and sales growth slowed compared to the first half, largely down to the vegan sausage roll being introduced in January. Shares have currently fallen over 5%.

Shares in Greggs plc (LON:GRG) were trading at -6.75% as of 11:18 BST Tuesday.

The British bakery chain said, however, that it sees food prices going up and sales growth slowed compared to the first half, largely down to the vegan sausage roll being introduced in January. Shares have currently fallen over 5%.

Shares in Greggs plc (LON:GRG) were trading at -6.75% as of 11:18 BST Tuesday.